3 Minute Economic Summary: April-May 2019

Key points

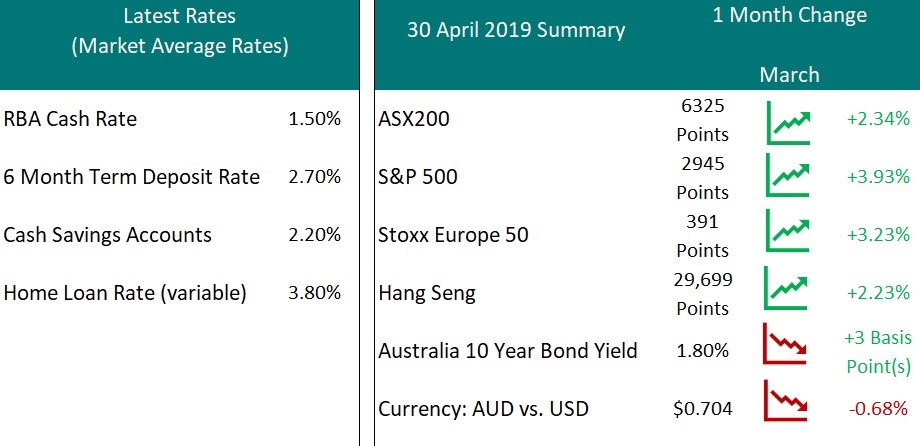

- Up to early May, global shares had continued to recover from the sell-off in late 2018. The US, was supported by stronger-than-expected economic data and a continued pause (or possible cessation) to increases in its interest rates.

- After this time, cautious optimism about a resolution to the the US – China trade talks turned negative following anti-China tweets from President Trump and the imposition of higher tariffs on a range of Chinese exports. This then resulted in a Chinese retaliation with new tariffs of their own. Despite this recent setback, the strong gains earlier in the year mean that year-to-date returns remain substantial.

- For world share markets, the global business cycle still looks solid, although 2019 is shaping up to be a bit weaker than 2018. The major risk is currently geo-political, and it is difficult to determine the outcome of the US – China trade talks. The impact could be significant, both on the upside and the downside.

- The global backdrop of higher trade tensions has had an impact on Australian shares, which have drifted down from their recent peak on 26 April after also rallying strongly. However, markets reacted very positively to the return of Scott Morison and the Liberal Party to government, given Labour was expected to win and bring with it negative tax ramifications for franking credits and negative gearing.

- The Australian business cycle has weakened, and the Reserve Bank is anticipated to provide at least one interest-rate cut, potentially as early as June. Additional cuts are to try and boost the slowing economy and help get inflation up into its targeted 2% to 3% band. Savers are anticipated to be receiving very low levels of bank deposit income for some considerable time.

- It is worth noting that the Australian economy is still growing, however listed Australian companies are likely to find it harder to grow their profitability.

- The Australian dollar has also dipped on expectations of a rate cut (which is good for Australian exports), however higher demand resulting in increases to commodity prices may see the dollar claw some of this back.

Altitude Financial Planning is a Corporate Authorised Representative of Altitude Financial Advisers Pty Ltd

ABN 95 617 419 959

AFSL 496178

The information contained on this website is general in nature and does not take into account your personal circumstances, financial needs or objectives. Before acting on any information, you should consider the appropriateness of it and the relevant product having regard to your objectives, financial situation and needs. In particular, you should seek the appropriate financial advice and read the relevant Product Disclosure Document.